Great breakdown.

The data mirrors what we’ve been seeing from our own merchant analytics at Popupsmart.

Over the past year, we’ve noticed a *steady migration of small to medium Shopify merchants* looking for leaner, more flexible setups. The main reasons they share with us echo your findings:

- Cost accumulation: Subscription + app + transaction fees often exceed initial budgets.

- Customization limits: Merchants want more control over design, checkout, and integrations.

- App dependency fatigue: Managing multiple apps for basic growth features becomes overwhelming and expensive.

Interestingly, as merchants grow, their priorities shift. Many who once valued Shopify’s simplicity now look for open-source or hybrid solutions that provide better cost control and ownership. On the other hand, we still see brands returning to Shopify later when they want stability, faster deployment, and a strong support ecosystem — confirming your “bidirectional migration” insight.

From a marketing tools perspective, we’ve also seen higher conversion performance when merchants pair lightweight, independent tools (like Popupsmart) with flexible platforms such as WooCommerce or BigCommerce. This independence helps reduce reliance on heavy app ecosystems while improving site speed and UX.

Quick context from fresh 2026 numbers:

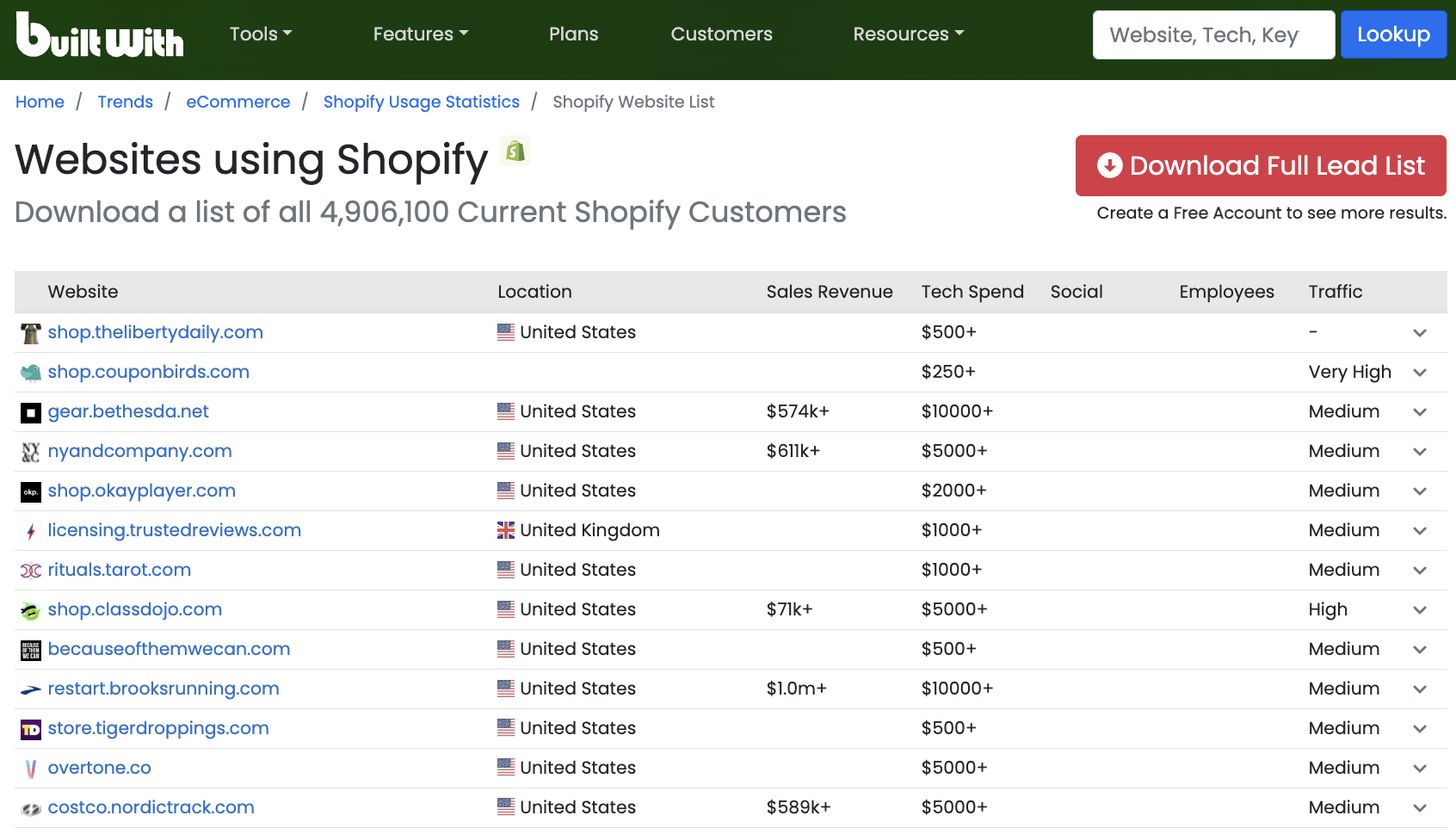

Shopify’s still massive around 2.84 million live stores worldwide right now (TechnologyChecker.io shopify technology detection data from late Feb/early March 2026), though BuiltWith picks up closer to 6.9 million when counting redirects and broader tech detections. Growth slowed a bit after the pandemic boom—18% YoY in late 2025, but slight dip quarter-over-quarter.

Our own tracking covers millions of companies on Shopify, everything from solo founders to big names like FedEx, Ford, Adobe (often on branded sub-stores or Shopify Plus). Shopify Plus itself powers roughly 41,000–42,000 distinct merchants (StoreLeads Feb 2026).

The US takes the biggest slice (~38–53% of stores depending on the tracker), then UK, Canada, Australia, with India picking up speed. DTC fashion, beauty, home goods still dominate the long tail—lots of micro-merchants with just a handful of products.

Bottom line: I agree 100%. Platform isn’t a forever choice—it’s about what fits your stage right now, not just day-one needs.

In short, I completely agree — platform choice isn’t final, it’s strategic. The best platform is the one that matches your current growth phase, not just your initial launch needs.